Overview of the dairy industry in Sri Lanka

The dairy industry has been a key focus in successive Governments, with a key objective repeatedly highlighted being to achieve self-sufficiency in milk products. The target year for the achievement of this objective appears to be a moving target, with the most recent goal being 2020. Despite this self-sufficiency goal, local production meets below 40% of the total domestic milk requirement, considerably below 80% levels in the 1970s. Therefore, presently, majority of the demand in milk products is met through imports, mostly from New Zealand and Australia. In 2015, local milk production amounted to 374 million litres, a 12.1% increase from the previous year. In comparison, imports of milk and milk products grew by 21.5% over the year. Over, the last decade, in 7 out of 10 years, imports of milk powder has grown at a higher pace than the growth in local production.

For the purpose of this report we will focus largely on Milk Powder and Fresh Milk (Liquid Milk) as they stand to be the most exposed to the effects of price controls and regulations. Consumers in Sri Lanka tend to prefer milk powder over liquid milk given its longer shelf life amid limited refrigeration facilities as well as a higher perceived nutrition and greater availability to the masses.

According to the most recent Household Income and Expenditure Survey conducted in 2012/13, the domestic household spent an average of Rs. 1,389 per month on milk and milk foods, which accounts for 8.9% of the total expenditure on food. Taking a closer look at Milk Powder specifically, the household spent an average of Rs. 1,036 per month. However, interestingly, over time, despite the expenditure on milk powder rising at 11.8% annually (Compound annual growth rate –CAGR) between the 2009/10 and 2012/13 survey periods, quantities consumed have reduced by 1.4% annually. This also holds true for the period between the 2006/07 and 2009/10 surveys. This indicates that while consumers spend more on milk powder, the quantity consumed is reducing.

Market Players

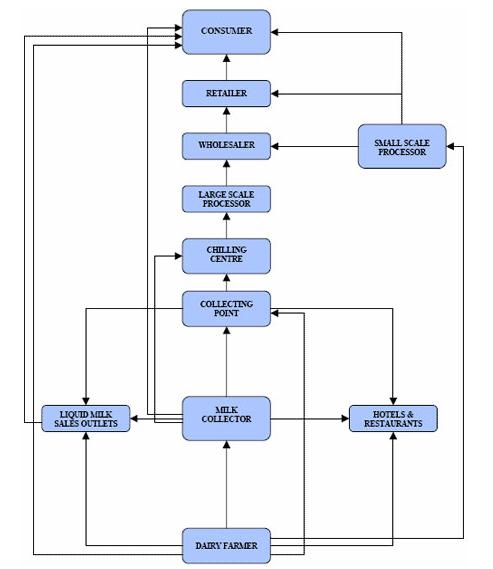

The dairy industry in Sri Lanka consists of multiple players along the supply chain. Broadly, the industry consists of Dairy Farmers, Milk Collectors, Producers or Processors, and the retailers. A more comprehensive breakdown of the several players in this industry is provided in Figure 1.

In terms of milk powder, Fonterra’s Anchor and Ratthi hold the largest market share according to market information, followed by Nespray (by Nestle Lanka PLC), Lakspray (by Lanka Milk Foods (CWE) PLC) and Maliban (by Maliban Milk Product Pvt Ltd). Other domestic players include Pelwatte (by Pelwatte Dairy Industries Ltd) and Highland (by State-owned, Milco Pvt Ltd).

In terms of Fresh Milk, the key brands are Anchor, Kotmale (by Cargills (Ceylon) PLC), Ambewela (by Lanka Milk Foods PLC), Highland and Richlife (by Renuka group).

The key players involved in milk collection and value addition to milk powder are Milco, Nestle, Lanka Milk Foods, Cargills and Pelwatte. Other players mentioned above are largely involved in packing and distribution of imported milk, although a select few also do engage in the production of fresh milk.

Figure 1 – Flowchart of Milk Industry

Source: FAO

History of price controls in the dairy industry

Price controls in the dairy industry appear to be commonplace, with impacts being felt from the source to the end-consumer. Much of these regulated prices and their constant revisions are intended to encourage domestic production and meet its overall objective of self-sufficiency as well as to shield consumers or producers from unfavorable movements in global whole milk powder (WMP) prices. The most visible price control in this sector is the Maximum Retail Price (MRP) imposed on Milk Powder, declared an essential commodity in Section 18 of the Consumer Affairs Authority Act No.9 of 2003 (Source: Government Information Centre). In addition to this, at the source, the farm gate price, which is the price a farmer receives for supplying fresh milk, is also controlled by the Government. Furthermore, the use of import duties and other taxes could also be considered forms of price controls in this industry.

Maximum Retail Price (MRP)

The MRP stands to be the most common form of price control instituted by Governments. In Sri Lanka, both imported milk powder and locally produced milk powder are subject to an MRP. However, importers generally face a higher MRP than local producers, with the aim of making locally produced milk more competitive and affordable to consumers.

Over the years, the MRP charged for importers and local produced has varied significantly, with revisions being seen almost annually. In 2010 and 2011, due to a significant increase in global WMP prices, the MRP of a 400g milk powder pack was raised by Rs. 19 and Rs. 20 each year respectively. Since then, the MRP of the 400g milk powder pack hit a high of Rs. 386 in 2014, once again driven by a surge in international prices reaching up to US$ 5,000/MT. However, WMP prices have dropped since then hovering around US$2,000 to US$ 3,000 levels for the past two years allowing the Government to reduce prices. As at the time of writing, the MRP in Sri Lanka stands at Rs. 325 and Rs. 295 for imported and locally produced milk powder respectively, unrevised since the 2015 Budget. Similar price revisions are also evident to 1kg milk powder packs.

Graph 1 – MRP of 400g Milk Powder Pack

Source: Ministry of Finance, news articles

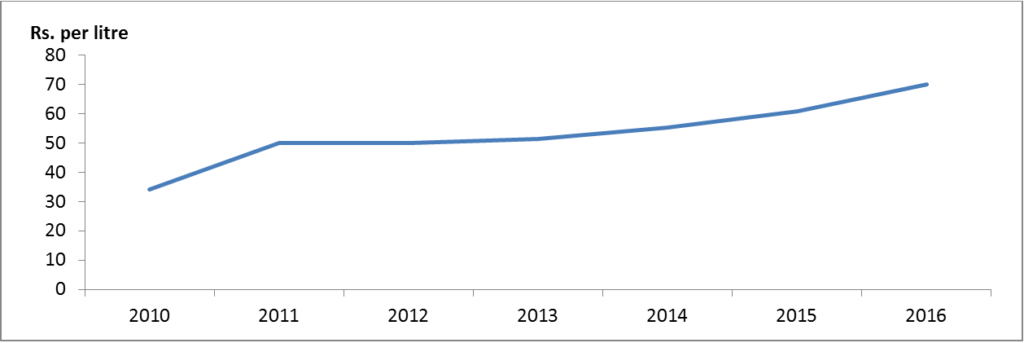

Farm Gate Price

While MRP is used to protect the interests of consumers and producers, the control of farm gate prices is largely aimed at encouraging domestic production and improving the quality of domestically produced milk. Since 2010, farm gate prices have doubled, rising to Rs. 70 per litre in 2016 from Rs. 34 per litre in 2010. In comparison, from 2010 to 2015, domestic production grew by 51%, corresponding to an annual growth of 8.6% (CAGR).

While the repeated revisions to the farm gate prices support farmers, it increases the cost of production for processors. According to the FAO (Food and Agriculture Organisation of the United Nations), farm gate prices are largely determined by state-owned Milco’s costs and thus, is used as a tool for this state-owned enterprise to manage its costs.

Graph 2 – Farm gate price

Source: Ministry of Finance

Import duties and sensitivity to tax changes

In addition to the MRP and Government-controlled farm gate prices, importers are further subject to adjustments in import duties. These tend to vary depending on the impacts of WMP prices on importers or follow the fiscal policies of the present Government. Most recently, in December 2016, it reduced the import duty by Rs. 55, immediately after reducing it by Rs. 35 in the November 2016 budget. The same budget also planned to tighten the belts of both importers and domestic producers, proposing to remove VAT exemptions on milk powder.

Sector Analysis

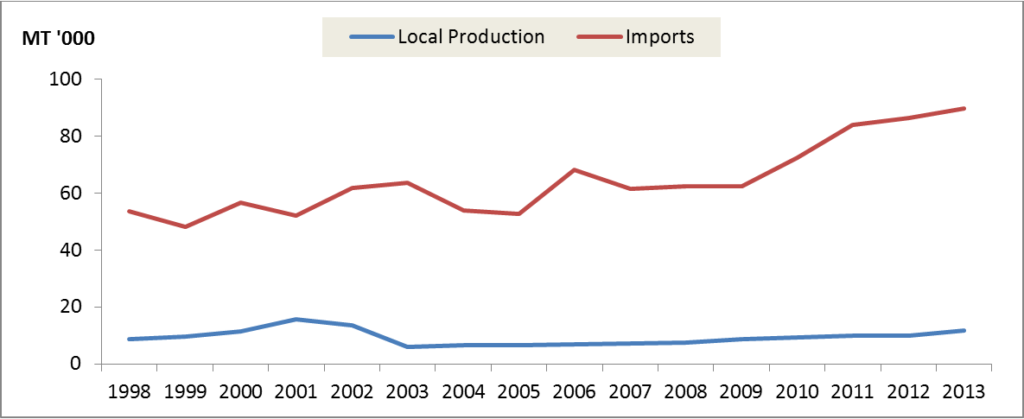

Local Production versus Imports

The dairy sector in Sri Lanka is dominated by imported products, with only a handful of domestic producers in comparison. It is not difficult to understand why being an importer of milk powder is more lucrative than producing locally. Firstly, given the shortage of milk produced domestically, with domestic production meeting only close to 40% of the total milk requirement, imports are a necessity and cannot be completely discouraged by the Government. Additionally, importers purchase its raw material at international prices and can gain an advantage when these prices moderate, as it currently is, conversely, they also incur higher costs when these prices rise. On the contrary, at certain times, importers can face greater adversity than domestic producers, particularly through the unpredictable revisions of import duties, which negate any benefits from global prices.

Nevertheless, given the vast variance between the quantities of milk powder imported against domestically produced milk powder, it could be argued that imports do not just meet the production gap but far surpass it.

Graph 3 – Powdered Milk: Local Production vs. Imports

Source: Department of Census and Statistics

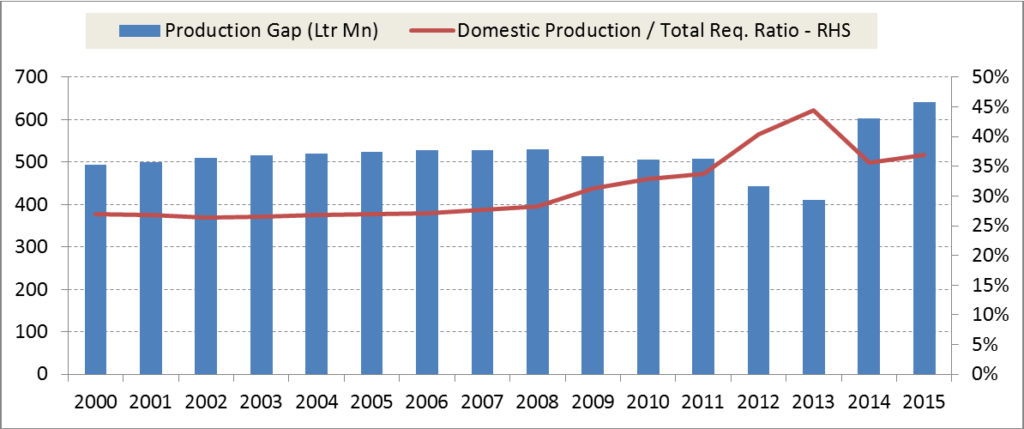

Graph 4: Domestic Production Gap vs. Total Domestic Requirement

Production Gap = Total Milk Requirement – Domestic Milk Production

Domestic production to Total Requirement ratio gives the percentage of total demand which is met by local production.

Source: Ministry of Finance

Input Costs

While it is apparent that due to government controlled farm gate prices domestic producers have no control over a significant portion of their raw material cost, whereas importers on the other hand are able to source from global markets essentially allowing them to manage their raw material costs, it could be argued that their exposure to movements in WMP prices could make their margins much more volatile than that of domestic producers.

However, through revisions of import duties and MRPs, the full effects of movements in global prices are not felt by importers. For instance, in periods where WMP prices surged such as in 2011 and 2013, the MRP of milk powder was increased to reflect this, however, the benefit of this was not fully passed on to importers as import duties were raised, exacerbating their difficulties. Local producers, on the other hand, were able to expand their margins further due to higher retail prices. As evident in Graph 4, these periods also helped to reduce the domestic production gap as well with the domestic industry benefiting from a milk shortage.

With WMP prices declining significantly since then, the MRP was also reduced. However, while importers are now exposed to considerably lower input prices, local producers are not compensated similarly with farm gate prices continuing to be increased. In fact, despite low WMP prices, duty waivers have been increased further to benefit importers. However, it is possible that the imposition of VAT on 1st November 2016 may have eroded this benefit.

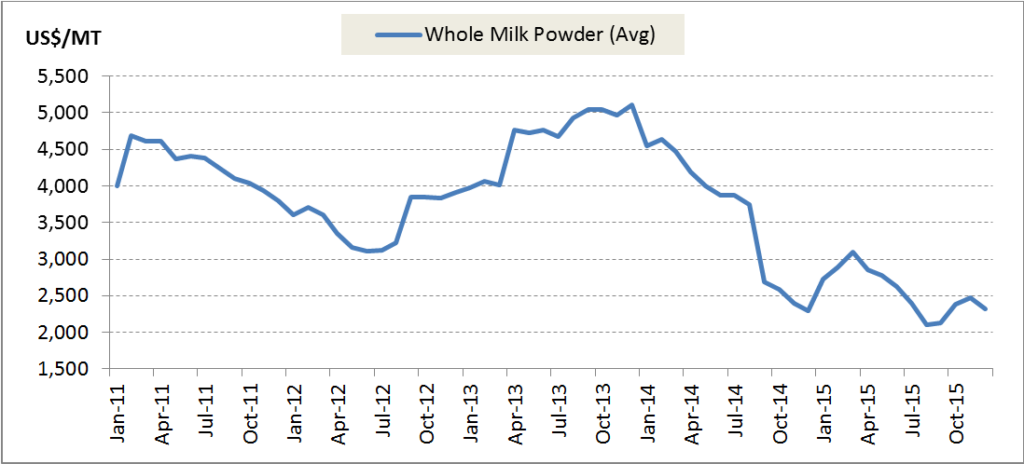

Graph 5 – Global Whole Milk Powder (WMP) prices

Source: Livestock Bulletin 2015(DAPH)

Yield of domestic production

As mentioned previously, the control of farm gate prices is expected to encourage domestic milk production. In addition to this, a number of other factors also contribute to growth in local production of milk, including the number of milking cows and facilities and training provided to farmers to increase the yield from cows.

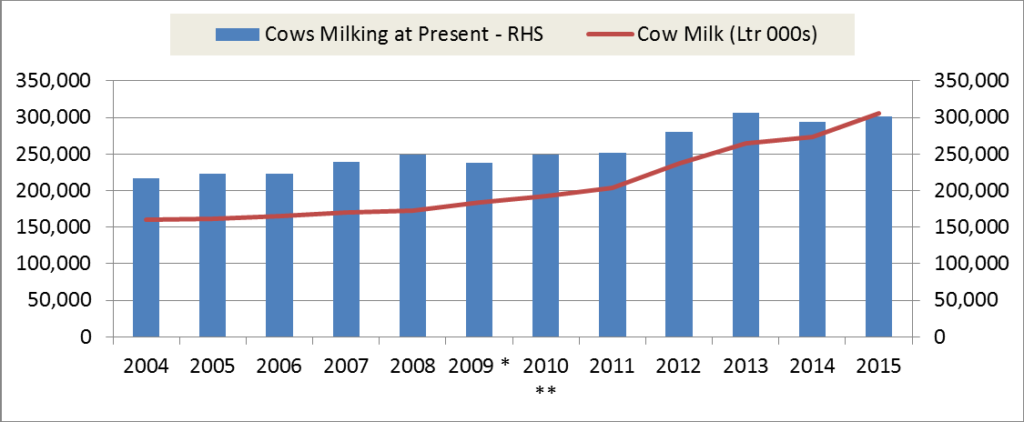

In the past three years, the numbers of milking cows have remained quite stagnant; however over the same period milk production has continued to increase. This could be attributed to technological advancements in breeds of milking animals, pasture developments, training and adoption of advance animal husbandry, management and milking techniques, etc. The government as well as the private sector have supported these developments, with the government also engaging in importing cows over the past few years.

Graph 6 – Cow milk production vs. Number of cows milking

Source: Department of Census and Statistics

* Excluding Killinochchi and Mulativu Districts

** Excluding Kilinochchi District

Profitability of Dairy producers/processors

Milco (Pvt) Lrd

Milco is the primary dairy state-owned enterprise, in addition to the National Livestock Development Board (which engages in issuing quality breeding materials to farmers at reasonable prices, establishment and maintenance of marketing outlets to supply quality farm products at reasonable prices and sale of fresh cow milk to the public). Milco is presently engaged in collecting, processing and distribution of milk in the country.

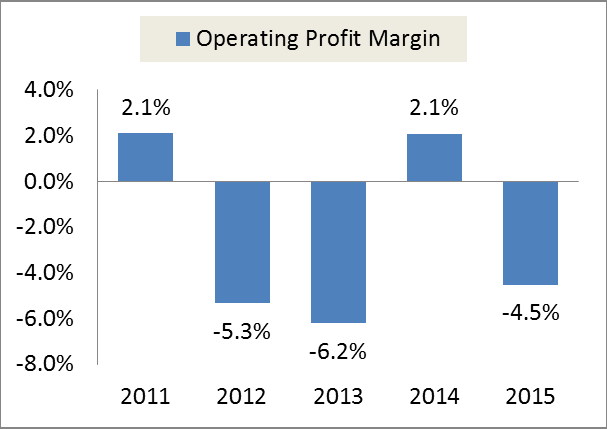

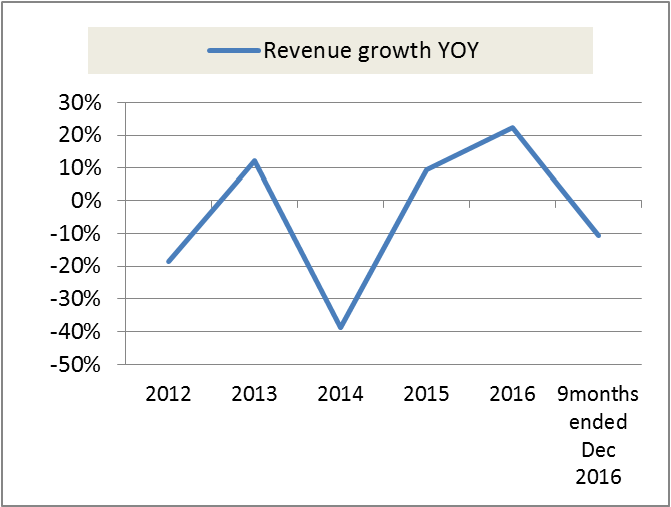

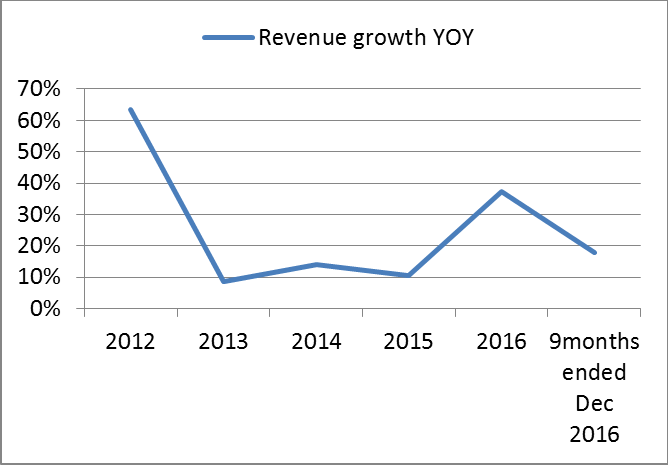

Analysis of Milco’s financial performance indicates that despite revenues growing positively through most years, it still incurs operational losses consistently. These losses have largely been attributed to the increase in farm gate prices, which resulted in rising direct expenses (particularly in FY2012 and FY2013) as well as capacity expansion activities (in FY2015).

On the other hand, the impacts of MRP revisions have also been evident in their margins, particularly in FY2014 where it attributed to increase in profits to the upward revision of the retail price. Meanwhile, the moderation in revenue seen in FY2015 is likely due to the steep reduction in the selling price during the year.

Graph 7 – Milco (Pvt) Ltd : Revenue growth vs. Profitability

Source: Ministry of Finance

Lanka Milk Foods (CWE) PLC

Lanka Milk Foods (CWE) PLC packages and distributes imported whole milk powder and skim milk powder- Lakspray and Lakspray Non-Fat, while its subsidiary Lanka Dairies (Pvt) Ltd manufactures and distributes UHT treated fresh milk and Non-Fat milk under the brand of Ambewela.

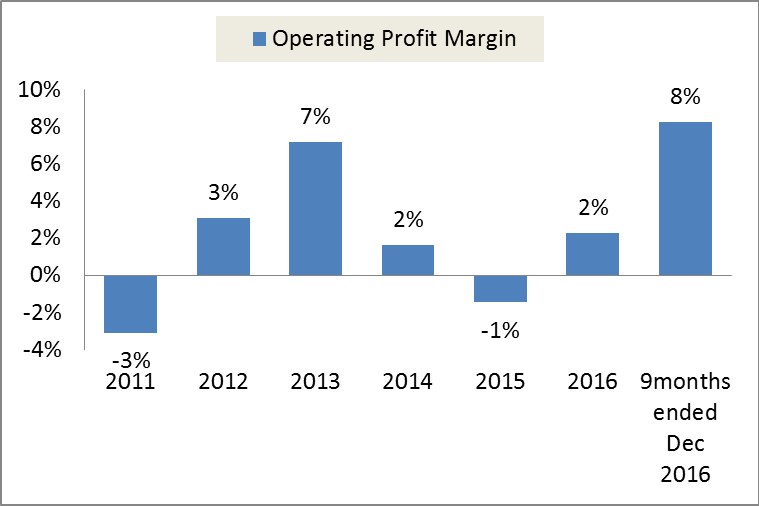

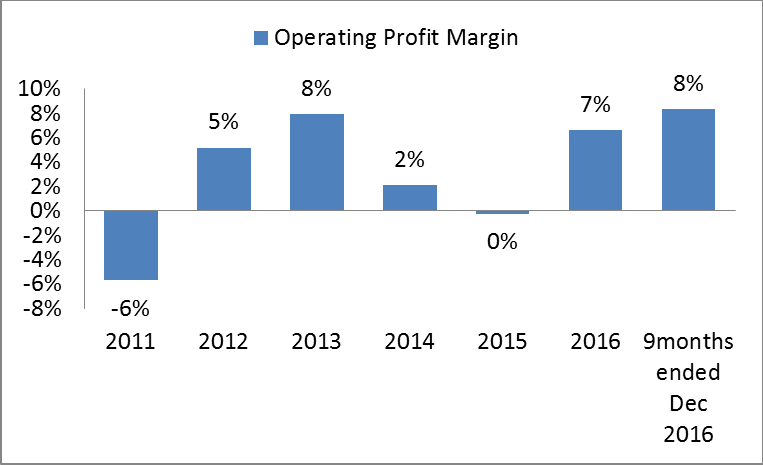

Analysis of its financial performance indicated that it is strongly impacted by all forms of price controls, i.e. farm gate prices, MRPs and import duties. Additionally, due to the import of milk powder by the company it is highly exposed to changes in international prices.

In FY2013, the government increased the retail price of milk powder, resulting in lower consumer spending on this commodity during the year. This was also amid rising global prices and increased import duties faced by the company. Despite these unfavourable conditions, the company managed to grow its revenue through a brand re-positioning exercise of Lakspray, and was also able to post profits owing to forward booking of milk powder stocks.

In FY2014, international market prices soared, however it was not reflected domestically as the Consumer Affairs Authority (CAA) did not revise its retail prices in a timely manner. This exerted pressure on the company’s margins, specifically on milk powder. Due to a shift in consumption patterns from milk powder to fresh milk, the liquid milk segment was, however, able to improve its revenues, despite poor margins.

During FY2015, international milk powder prices began to decline. However, the local authorities immediately responded with increased duties on milk powder imports, while also reducing the MRP. This created a very unfavourable situation for the industry. During this period, the operating profit margins of the milk powder segment contracted to -1%. This was despite a revenue increase observed due to lower prices increasing consumption of milk powder.

With the subsequent decline in global milk powder prices, the company was able to improve its margins, both in powdered milk and liquid milk. However, the impact of the VAT could limit these benefits.

Graphs 8, 9 – Performance of Powdered Milk

Graphs 10,11: Performance of Liquid Milk and others

Source: Company Annual Reports

Industry Perspectives on Price Controls

Overall, most producers and retailers have publicly made known their displeasure with the use of price controls. A few of the insights gathered from annual reports as well as conversation with industry stakeholders gave further clarity to this notion.

Fresh Milk Producers

“The successive increases in farm gate prices of fresh milk have made local dairy farmers uncompetitive against the cheaper imported milk powder. Milk powder is an essential nutrition component in the diet of a majority of Sri Lankans and the Company appreciates the necessity to maintain lower prices in view of health and nutrition-intake concerns. However the context is counterproductive to the effective expansion of local dairy production due to the prohibitive pricing that stems from the high raw material and processing costs.”

– Cargills (Ceylon) PLC, Annual Report 2014/15 and 2015/16

Milk Powder Importers

“The year under review proved challenging for the milk powder sector, with the unprecedented hike in milk powder prices in the international market. No sooner the prices started decreasing in the international market, the government authorities counteracted by increasing the import duty Immediately. In addition to this, the Consumer Affairs Authority brought down the selling price of milk powder thus causing a very unfavourable situation to the industry.”

– D H S Jayawardena, Chairman, Lanka Milk Foods (CWE) PLC, Annual Report 2014/15

“The shortage of high quality raw milk to meet the increasing liquid milk demand will continue to pose an obstacle to meeting the needs of the sector. Simultaneously, the increasing import duty on imported milk powder will continue to make milk powder a luxury and not a necessity, as should be the case for the citizens of the country. The maximum retail price imposed by the government authorities serves to have a detrimental effect on the selling price of the final product, thereby affecting the accessibility to a nutritious essential product such as milk”

– S. C. Jayawardena, Director, Lanka Milk Foods (CWE) PLC, Annual Report 2014/15

“The profitability of the powdered milk arm suffered during the year due to the refusal by the Consumer Affairs Authority to allow companies engaged in the marketing and distribution of powdered milk to hike their prices in keeping with the global price rise in the rates of powdered milk. This ongoing and unfavourable status quo for the last two years is eroding the profitability of the powdered milk business in the country and gives rise to an urgent need for the renewed appraisal of price structures. We have made several recommendations to the appropriate authorities to consider the plight of powdered milk companies.”

“I am hopeful that the government authorities and the Consumer Affairs Authority will take a well-informed decision to allow price increases in line with rising global prices of powdered milk in order to ensure a level playing field in the industry.”

– S. C. Jayawardena, Director, Lanka Milk Foods (CWE) PLC, Annual Report 2013/14

Other milk powder importers also echoed this sentiment, noting that price advantages from global price movements did not have their desired impacts as import duties are used to negate this benefit. Moves like this have even convinced some importers to stop imports and source milk locally, despite the plethora of problems in this segment as well.

Importers also expressed displeasure in the fact that the maximum retail price for this product has remained unchanged for the past two years, despite several changes in both global as well as domestic markets. The ad-hoc implementation of VAT beginning in November 2016 was a further blow to this industry.

Sector experts also pointed out the importance of imports as it believed that self-sufficiency was not a realistically achievable target for Sri Lanka. Both given the shortage of milk production in Sri Lanka, due to poor productivity, as well as constraining supply factors such as the limited landmass in the country, to meet the total demand requirements (estimated to be between 80,000 – 85000 MT according to industry sources).

“Sri Lanka plans to increase its domestic dairy production to 100% self-sufficiency by 2016. This is a challenging task, given the current state of the industry which merely supplies approximately 35% of the domestic requirements. Moreover, the limited landmass in Sri Lanka poses a Herculean challenge to make the country self sufficient in liquid milk.”

– D H S Jayawardena, Chairman, Lanka Milk Foods (CWE) PLC, Annual Report 2012/13

Responding to the effects of VAT hikes which came into effect in November 2016, Fonterra Brands Sri Lanka and Indian Subcontinent Managing Director Sunil Sethi expressed the following sentiments at a forum:

“It is not the way to go about it. We will be happy if we can source every drop of milk from this country. But currently we (local sourcing) can meet only 30 percent of the demand. But by curbing imports, we will run out of milk. Needed is an end-to-end solution to grow the local dairy industry, … Like it or not, imports are here to stay. And we prefer if it stayed till we are able to develop our local dairy industry to fulfil our demand,”

(Source: Daily Mirror)

Local Producers

Local producers are greatly affected by price controls, both at source, as they purchase milk at farm gate prices, as well as at the point of sale, with the MRP being fixed. This leaves them with minimal control over costs and profits, dissuading them from local production while also constraining innovation, which is a vital factor if Sri Lanka is to improve this industry. Further, given the almost annual increases of farm gate prices, farmers have no motive to improve productivity and will continue to remain at present levels.

Local producers further question the contradictory motives of the government which accommodates policies that allow imports to flood the market while holding onto objectives of self-sufficiency. This excess supply created in the market through imports suggests that prices should be lower, despite local producers being unable to sell at such prices.

Conclusions

Examining the market factors and players, and following careful analysis from views provided by varied stakeholders in the industry, it is evident that there is a disconnect with the aim of achieving self-sufficiency and the role of price controls, both at a retail level, with the use of MRPs, and at a farm gate level.

The removal of the MRP would allow for a higher level of healthy competition among both importers and local dairy manufacturers, allowing market forces to decide prices. In terms of controlling farm gate prices, it is necessary that the government consider the needs of 20 million consumers above the 200,000 farmers who are the sole beneficiaries of this control. This would allow greater predictability and transparency of costs and revenues among industry players.

It is also necessary for the government to recognise that given several supply constraints, the objective of self-sufficiency is not realistically attainable in a Sri Lankan context. Thus, authorities should to recognise the importance of imports in meeting the growing demands of consumers, and implement well-thought out measures to level the playing field between importers and domestic producers.