Sri Lanka’s state owned enterprises are consuming hundreds of billions of rupees in capital, weakening government finances, burdening the people, running up large losses and are undermining national savings, analysis of available data shows.

Following reforms and governance improvements that started under the Chandrika Kumaratunga administration, the larger state banks are no longer showing losses, though they are still lending to loss making state enterprises against Treasury guarantees.

However, smaller lenders remained dens of corruption and a route for political henchmen to steal public funds by defaulting on loans.

SME Bank and Lankaputhra Bank, the last two state banks set up in Sri Lanka, collapsed so fast under the weight of bad loans that questions have been raised whether they were built specifically to enable lending to politically connected borrowers who could no longer borrow and default on state-run People’s Bank and Bank of Ceylon following reforms.

The Agriculture and Agrarian Insurance Board, continue to draw budget support. In the case of Sri Lanka Insurance, which was returned to the government after a brief period of private management, there have been allegations of fraud in related entities, although the parent firm constinues to report profits.

Fiscal Drag

The situation with non-financial public enterprises is worse. Many continue to be a big burden on the tax payer and also help de-stabilize the economy hurting ordinary people.

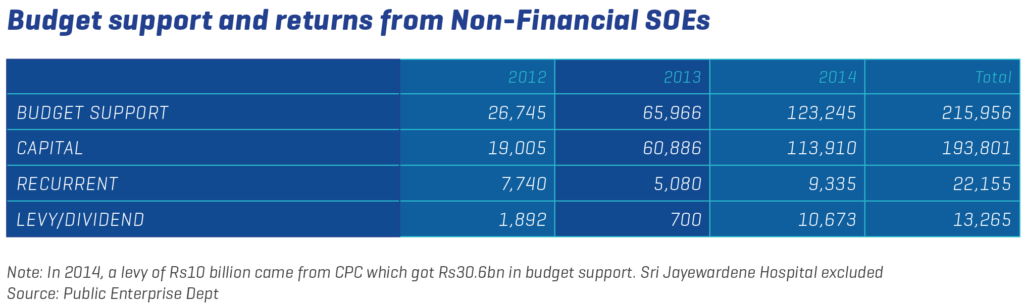

In the three years to 2014, of the 55 state entities monitored by the Public Enterprises Department of the Treasury, 42 state entities received a total of 215 billion rupees in budget support. Budget support climbed from 26.7 billion rupees in 2012 and 65.9 billion rupees in 2013 to 123.2 billion rupees in 2014.

The budget funds given to state enterprises in 2014 is equivalent to every household paying 24,100 rupees to keep the non-financial state entities afloat. To put this in perspective, around 40 percent of Sri Lanka’s 5.1 million households earn less than 24,000 rupees a month.

Despite hundreds of billions of rupees being pumped into these enterprises, they bring hardly any return to the budget. In 2012, non-financial public enterprises got 67.46 billion rupees in budget support of which 7.7 billion rupees was for current spending.

Only five enterprises paid dividends and levies totalling 1.89 billion rupees in that year. In 2013, people injected 65.9 billion rupees from the budget to these entities of which 5.0 billion rupees were for current expensive. Only five enterprises paid 700 million rupees in levies and dividends.

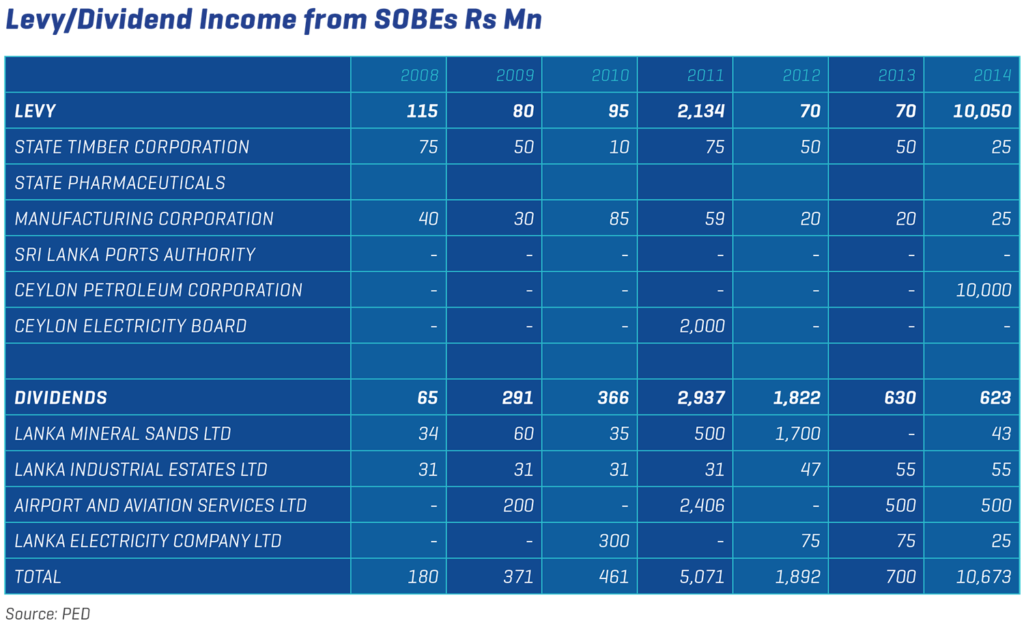

In 2014 an unprecedented 123.2 billion rupees were injected from the budget of which 9.3 billion rupees was to cover routine, recurrent spending. Dividends and levies were only 10.673 billion rupees. Out of that, 10 billion came from Ceylon Petroleum Corporation (CPC) which was making profits due to falling crude prices. But in the same year CPC got 30.6 billion rupees in budget support to cover earlier losses and strengthen its balance sheet.

The dismal performance of Sri Lankan state enterprises is in sharp contrast to about two billion Singapore dollars paid into the budget each year for the last three years by Temasek Holdings, which owns major public enterprises in that country. State enterprises perform well in Singapore. Electricity prices are also adjusted monthly and there is competition in generation.

For the purpose of statistics, non-commercial state enterprises are classified as ‘private sector’ when national savings are computed, giving the erroneous idea that Sri Lanka’s ordinary citizens do not save as much as other Asian peers. Their losses therefore drag down Sri Lanka’s private savings rate and therefore the domestic and national savings rate, giving misleading information to policy makers and analysts.

Domestic private savings fell from 21.4 percent in 2010 to 16.5 percent of gross domestic product in 2011. In 2011 for example losses of two state energy enterprises alone totalled over 1.5 percent of gross domestic product.

Circular Debt and Economic Vulnerabilities

State energy enterprises and the state banks together form a nexus of vulnerability for Sri Lanka’s economy and the stability of the currency which is related to the same phenomenon.

To win votes politicians control the tariffs of energy utilities when world market prices rise. The energy utilities are forced to sell at a loss, the losses being funded by banks.

Large losses in the Ceylon Electricity Board (CEB) and Ceylon Petroleum Corporation (CPC) has helped trigger balance of payments crises in 1999/2000, 2009, and 2011/2012.

During the 2011 crisis, bank-financed cash flow deficits at CPC totalled 117.5 billion rupees. At Ceylon Electricity Board, it was 10.8 billion rupees.

These numbers understate the actual impact of losses at the CEB, because through a circular process, its losses accumulate as debt elsewhere.

CPC’s large losses in 2011 partly came from selling fuel at a loss to the CEB. The CPC in turn is effectively used by other state agencies to finance their losses, as fuel bills remain unpaid for extended periods. SriLankan Airlines and Mihin Air are notorious for delaying payments to the CPC. In 2011, in addition to selling fuel at a loss, the CPC also extended 8.8 billion rupees in credit to the CEB.

When state banks are compelled to finance losses at state enterprises, investible funds collected from the public are misused for consumption.

Economic analysts have pointed out that when bank credit surges and the loans are re-financed by the central bank credit (printed money) or through discount window operations, and not with deposits raised from the public, balance of payments problems occur leading to currency collapses.

Because some banks are state-owned, they finance the CPC and CEB disregarding prudential rules such as single borrower limits, or the likelihood of default. To safeguard themselves Treasury guarantees backed by the future earnings and taxes of ordinary people are given.

However, if the banks or the energy utilities were private entities; with pricing freedom for energy utilities and freedom for bank management to extend credit under standard prudential rules; this nexus of vulnerability cannot continue.

It can be seen that Lanka IOC, an Indian state firm, took steps to minimise losses by refusing to sell kerosene at all in one instance and unilaterally raising diesel prices on another occasion without taking more loans to fund losses and de-stabilize the credit system.

If banks refused to give credit under standard prudential rules, the utilities would be selling oil at cost which in turn would have reduced the spending power of consumers and reduced non-oil imports, protecting the rupee and the balance of payments.